Your AI strategy could be destroying your valuation.

When we went through due diligence for our PE exit, I expected the usual questions: Revenue growth. Customer retention. Tech debt.

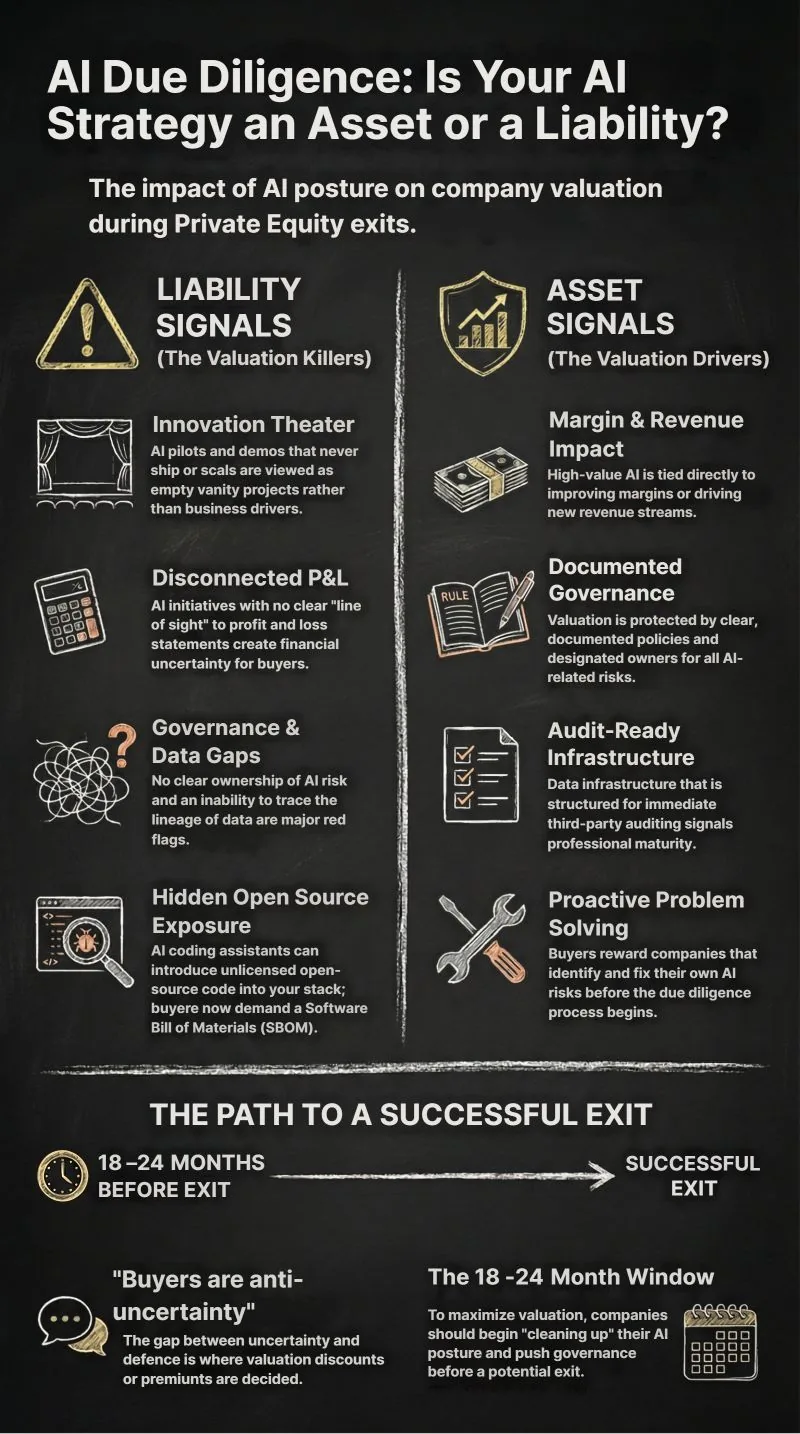

Your AI strategy could be destroying your valuation. Here's how to tell.

When we went through due diligence for our PE exit, I expected the usual questions: Revenue growth. Customer retention. Tech debt.

What I didn't expect was how much AI posture mattered. Not whether we had AI, but whether our AI was a liability or an asset.

Liability signals:

-

AI initiatives with no line of sight to P&L

-

"Innovation theater", pilots that never scale, demos that never ship

-

No governance framework, no one can explain who owns AI risk

-

Data lineage gaps, can't trace where data came from, access control

-

Hidden open source exposure from AI tooling

That last one caught me off guard. With AI coding assistants everywhere now, buyers are asking: do you actually know what open source is in your stack? What's your license exposure?

If your answer is "I think so" instead of "yes, here's the SBOM", that's a red flag.

Asset signals:

-

AI tied directly to revenue or margin improvement

-

Clear governance with documented policies and owners

-

Data infrastructure that's audit-ready

-

Proactive risk management, you found the problems before they did

The gap between these two positions is where valuation discounts happen.

Buyers are anti-uncertainty. They want to see you've thought through the risks and can defend your position.

If you're 18-24 months from a potential exit, the time to clean this up is now. Not during diligence.

In my next post, I'll share the 7-area AI due diligence checklist PE firms are starting to use.